Introduction

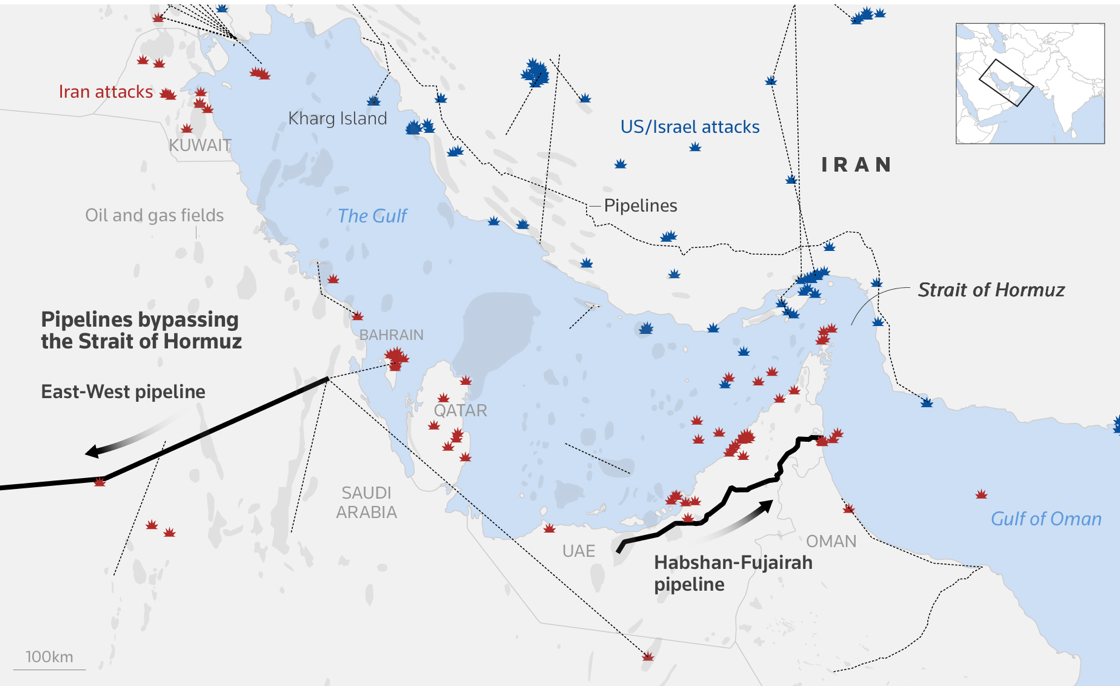

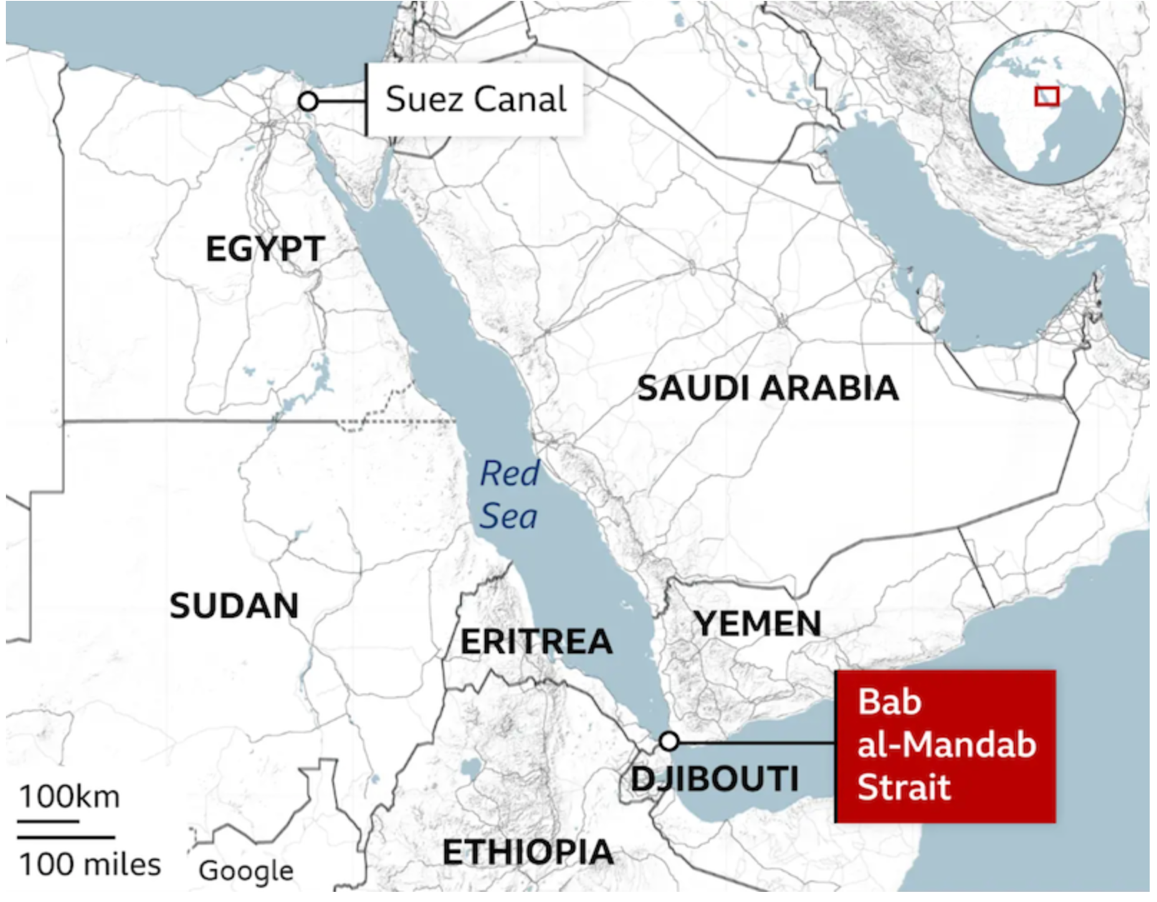

Modern wars in the Middle East rarely remain confined within national borders. Because the region sits astride the world’s most important energy and trade routes, military escalation there often translates directly into global economic disruption. The current conflict involving the United States, Israel, and Iran vividly illustrates this dynamic. From the beginning, the war had a naval and maritime dimension, and this aspect may well expand further. This is because two strategic chokepoints—the Straits of Hormuz and Bab al-Mandab—which serve as critical arteries for global oil and commercial shipping, could both become blocked if the Houthis reenter the fray. Already, Iran has effectively imposed a selective closure of the Strait of Hormuz, allowing only tankers aligned with or acceptable to the Iranian regime to transit, thereby weaponizing access to one of the world’s most vital economic corridors. The Houthis in Yemen have not yet disrupted maritime traffic through the Bab al-Mandab, but they retain the capability to threaten Red Sea shipping and global commerce as they did in 2024 and 2025. Simultaneous closure of both straits could pose severe consequences for global energy markets, trade flows, and international security.

The Middle East’s maritime routes already hold extraordinary geopolitical and economic significance before the U.S.–Israeli war against Iran began. The region sits at the center of the global energy transport system, linking major hydrocarbon producers in the Persian Gulf with energy-hungry markets in Asia and Europe. Prior to the outbreak of the war, oil flows through the Strait of Hormuz averaged approximately 20.9 million barrels per day, representing roughly 20% of global petroleum consumption and over 30% of seaborne oil trade.

In addition to crude oil, the strait also serves as a critical artery for natural gas, with around 20% of global liquefied natural gas (LNG) trade—particularly exports from Qatar—transiting this narrow waterway. Beyond Hormuz, the broader regional network—including the Bab al-Mandab Strait and the Suez Canal—facilitate the movement of an additional 8–9 million barrels per day of crude and refined products toward European markets, underscoring the interconnected nature of these chokepoints in sustaining global energy and economic flows.

The stability of this handful of narrow waterways is a cornerstone of both global economic security and great-power strategic planning and a core driver of great-power military presence in the region.

The Strategic Challenge in the Strait of Hormuz

The Strait of Hormuz is a narrow maritime chokepoint connecting the Persian Gulf to the Gulf of Oman and the Arabian Sea. At its narrowest navigable point, the strait is roughly 35 miles wide, making it both highly efficient for global trade and exceptionally vulnerable to disruption.

Since the outbreak of the war, Iran has relied on a calibrated strategy of maritime pressure in the Strait of Hormuz designed less to impose a total blockade than to raise the cost and risk of commercial navigation through a mix of missile launches, armed drone activity, naval harassment, and the threat of fast boat swarming and mine warfare. This approach reflects an asymmetric doctrine: by exploiting the strait’s narrow geography and proximity to Iranian territory, Tehran can disrupt confidence in shipping without sustaining continuous high-intensity operations. Even limited incidents—such as near-misses, temporary seizures, or credible mine threats—have produced immediate behavioral shifts in global shipping markets. Tanker operators have slowed or suspended transits, while war-risk insurance premiums for Gulf routes have skyrocketed, in some cases increasing from around 0.2% of vessel value to between 1.0 and 1.5 percent, significantly raising transportation costs.

The Houthi Threat in the Red Sea

The maritime risks could intensify dramatically if the Houthis in Yemen enter the conflict in support of Iran. The group controls much of Yemen’s western coastline along the Red Sea, allowing it to threaten shipping through the Bab al-Mandab Strait, a chokepoint only about 18 miles wide at its narrowest point and a critical link between the Indian Ocean and the Suez Canal.

Rather than imposing a traditional naval blockade—which would require capabilities beyond those of a non-state actor—the Houthis would likely pursue a strategy of sea denial, aiming to raise risk levels to the point that commercial shipping becomes too dangerous and economically or operationally unviable. Over the past decade, the group has developed a diverse arsenal of asymmetric maritime capabilities, including anti-ship cruise missiles (such as variants of the C-802), one-way attack drones, explosive unmanned surface vessels (USVs), and naval mines, many of which are derived from or influenced by Iranian systems. These systems are particularly effective in the Red Sea environment, where coastal launch sites can exploit mountainous terrain for concealment and the narrowness of shipping lanes limits evasive maneuvering.

Several escalation scenarios can be envisioned if the Houthis actively join the conflict. In a low-intensity scenario, the group would conduct sporadic drone and missile strikes against commercial vessels or near shipping lanes, sufficient to trigger sharp increases in insurance premiums and rerouting of traffic without sustained interdiction. This pattern has precedent: even limited Houthi attacks in 2023–2024 led to a 40–50% drop in Red Sea container traffic and forced major shipping lines to reroute vessels around the Cape of Good Hope, adding 10–14 days to transit times.

In a medium-intensity scenario, the Houthis could combine missile and drone strikes with the deployment of naval mines and explosive boats, creating a persistent threat environment that disrupts traffic. Mining operations, even if limited, would have outsized effects because mine countermeasure operations are slow and resource-intensive, often requiring specialized naval assets and international coordination. The mere possibility of mines can effectively close a shipping lane for commercial operators due to liability and insurance constraints.

In a high-intensity escalation scenario, potentially coordinated with Iranian actions in the Strait of Hormuz, the Houthis could attempt sustained attacks on multiple vessels, targeting not only tankers but also container ships and naval escorts. This could include coordinated salvos of missiles and drones designed to overwhelm defensive systems, combined with swarm attacks using fast boats or unmanned vessels. In such a case, the Red Sea could become an active combat zone, forcing the United States and its allies to deploy significant naval forces to secure the corridor, including air defense destroyers, mine countermeasure ships, and continuous aerial surveillance. Even under such protection, shipping throughput would likely decline sharply, and global supply chains would face severe disruption.

From a strategic perspective, the Houthis’ ability to threaten the Bab al-Mandab would effectively open a second maritime front in the conflict, amplifying pressure on global energy and trade flows already strained by tensions in the Persian Gulf. The key insight is that the Houthis do not need to physically close the strait to achieve strategic impact; by injecting uncertainty and risk into one of the world’s most critical shipping lanes, they can generate disproportionate economic and geopolitical consequences. This underscores how relatively low-cost asymmetric capabilities, when applied to geographically constrained chokepoints, can reshape global trade dynamics and force major powers into costly and complex maritime security operations.

Tehran’s Defiance and Global Energy Risks

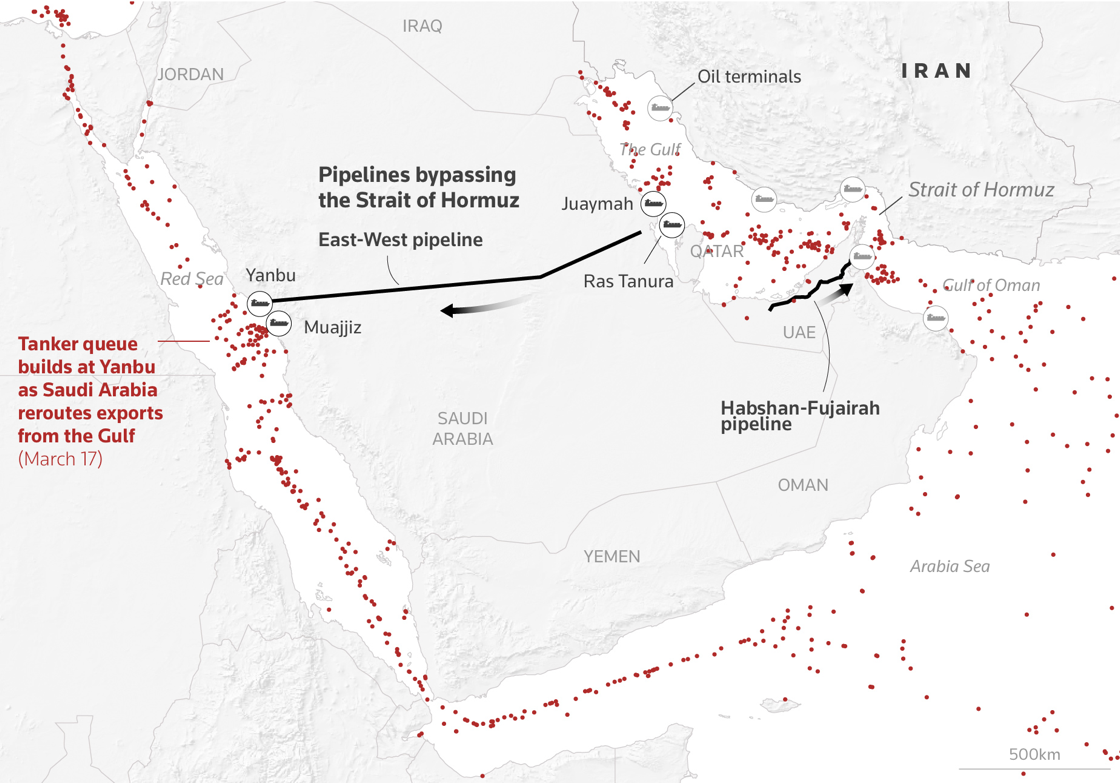

The crisis has exposed the structural fragility of highly concentrated maritime energy routes and accelerated strategic thinking about diversification and risk mitigation in global production and supply chains. In response, producers in the Gulf have increasingly turned to bypass infrastructure. Saudi Arabia’s East–West Crude Oil Pipeline (Petroline), which runs to the Red Sea, has an estimated capacity of 5–7 million barrels per day, while the UAE’s Abu Dhabi Crude Oil Pipeline can transport around 1.7 million barrels per day to the port of Fujairah outside Hormuz. However, even at full capacity, these routes can only offset a small portion of Hormuz flows, underscoring the structural limits of current regional alternatives. This has led analysts to emphasize broader diversification strategies, including overland corridors such as the Baku–Tbilisi–Ceyhan (BTC) pipeline and the expansion of the Trans-Caspian “Middle Corridor,” which aim to connect Central Asian and Caspian energy supplies to European markets while bypassing both the Persian Gulf and Russia.

The disruption of maritime routes has particularly acute implications for East Asian economies, which are structurally dependent on imported hydrocarbons transported through these chokepoints. Countries such as Japan and South Korea rely on the Middle East for over 70–90% of their crude oil imports, much of which pass through Hormuz, making them highly vulnerable to supply disruptions and price shocks. China, by contrast, is often described as relatively less exposed—not because it is insulated from disruption, but because its economy is less oil-intensive per unit of GDP and more diversified in supply sources. According to the International Energy Agency, China’s oil intensity (i.e., oil consumption relative to economic output) is significantly lower than that of advanced industrial economies, reflecting structural shifts toward manufacturing efficiency, electrification, and alternative energy.

In addition, China has diversified its supply through pipelines from Russia and Central Asia—such as the Eastern Siberia–Pacific Ocean (ESPO) pipeline—and has built substantial strategic petroleum reserves. Nevertheless, China still imports roughly 70% of its crude oil, and about 40–50% of those imports transit the Strait of Hormuz, meaning it remains highly exposed to maritime disruptions even if its macroeconomic sensitivity is somewhat lower.

At the same time, the energy market response to the crisis is pushing toward broader structural adjustments. Countries heavily dependent on Gulf energy flows are accelerating investments in LNG import terminals, diversified supplier networks, and strategic petroleum reserves to buffer against episodic chokepoint disruptions. The crisis has also reinforced long-term transitions toward renewable energy, electrification, and hydrogen, particularly in Europe and East Asia, as a means of reducing reliance on imported hydrocarbons vulnerable to geopolitical shocks. In this context, Tehran’s defiance—rooted in geography and asymmetric capabilities—has reshaped global energy security from a narrow focus on production volumes to a broader strategic concern with logistical geography, redundancy, and risk dispersion. The conflict demonstrates that in the 21st century, energy security depends as much on the resilience of transport networks and supply chains as on the availability of resources themselves. Building on this shift toward redundancy and risk dispersion, the disruption of maritime energy routes has important and asymmetric implications for both Russia and Europe, reshaping their economic incentives and geopolitical positioning.

For Europe, the crisis reinforces structural vulnerability despite efforts to diversify away from Russian hydrocarbons since 2022. Even after reducing direct pipeline dependence on Russia, Europe remains exposed to global price shocks because oil is a fungible commodity traded in integrated markets. Consequently, supply disruptions in the Gulf have translated into higher import costs, with oil prices rising above $100 per barrel during peak tensions, feeding directly into inflation, industrial costs, and fiscal pressures across European economies. This dynamic complicates Europe’s post-Ukraine energy transition by increasing the cost of both fossil fuel imports and the capital-intensive shift toward renewables.

For Russia, by contrast, the disruption creates a more complex but potentially advantageous economic environment. As one of the world’s largest oil exporters, Moscow benefits directly from higher global prices, even if export volumes remain constrained by sanctions: for every $10 increase in oil prices, Moscow can generate $2.8 billion in additional revenue for Russian exporters and its war effort.

This effect has been particularly pronounced in the current crisis, where price spikes driven by Gulf instability have increased the value of Russian crude exports, especially to Asian markets such as China and India. Data from the Centre for Research on Energy and Clean Air indicates that Russia has continued to earn hundreds of millions of euros per day from fossil fuel exports despite sanctions, with price increases offsetting discounts imposed on Russian crude.

Additionally, considering soaring oil prices and supply anxieties caused by disruptions in the Strait of Hormuz, the United States temporarily lifted sanctions on Russian oil exports in mid-March 2026 as a market-stabilization measure. On March 12, 2026, the U.S. Treasury issued a 30-day waiver and general license allowing the purchase and delivery of Russian crude and petroleum products that were already loaded on tankers at sea, a move aimed at increasing available global supply to help calm energy markets shaken by the Iran conflict. Officials said the waiver would last until approximately April 11, 2026 and would apply to an estimated 124–128 million barrels of Russian oil already in transit. The decision drew criticism from European leaders and Ukraine’s president, who warned that easing sanctions could funnel significant revenue to Moscow, with a rough estimate of $10 billion in potential additional war resources. This sanction waiver marks a significant, if temporary, reversal of earlier U.S. policy that had sought to economically isolate Russia following its 2022 invasion of Ukraine through restrictions on oil exports and associated maritime services. The timing of the waiver reflects Washington’s prioritization of short-term price stability, even at the risk of bolstering Russia’s oil export earnings. Kremlin officials themselves framed the waiver as evidence of shared interests in stabilizing energy markets and acknowledged that Russian volumes would be essential in addressing shortages.

However, both the temporary nature of the waiver and widespread opposition from U.S. allies underscore the tension between immediate energy market pressures and longer-term strategic objectives aimed at sustaining economic pressure on Moscow. At the same time, the crisis accelerates structural shifts in trade flows that favor Russia’s eastward reorientation. As Europe continues to reduce direct dependence on Russian energy, Moscow has deepened export relationships with Asia, particularly China and India, using alternative shipping networks and “shadow fleet” tankers to bypass restrictions. Disruptions in traditional maritime routes further incentivize this diversification, reinforcing a bifurcation of global energy markets into partially segmented blocs.

Implications for U.S. Policy and Alliance Dynamics

The closure and effective shutdown of the Strait of Hormuz has highlighted divergent impacts and strategic options for the United States, even as America’s relative vulnerability to Gulf energy disruption remains lower than that of many Asian and European states. Structurally, U.S. dependence on oil imports from the Middle East is modest compared with past decades; widespread domestic production and diversified import sources mean that only a small fraction of U.S. oil consumption historically came directly through Hormuz, in contrast to about 20 million barrels per day that transit the strait under normal conditions. However, the conflict has driven oil prices sharply higher—Brent crude has surged above $100 per barrel—affecting U.S. gasoline prices and inflationary pressures at home. This has contributed to political headwinds for the administration, as higher energy costs tend to erode consumer confidence and raise concerns among voters and lawmakers. These effects occur even if the United States is less directly dependent on Gulf supply, because global oil benchmarks influence domestic energy prices and broader economic conditions.

Faced with a near closure of Hormuz, President Trump has attempted to build an international coalition to reopen the strait, framing this as both a security imperative and a shared burden for nations dependent on Gulf oil. Trump has publicly called on NATO members and other major users of Hormuz oil—including France, the United Kingdom, Japan, South Korea, and even China—to deploy naval assets to secure the waterway and escort commercial shipping. Despite these calls, most U.S. allies have declined to commit warships. European leaders have emphasized non-military, diplomatic efforts to reopen the route and have rejected participation in combat operations, while Japan and Australia have indicated reluctance to send naval forces into an active conflict zone. Trump has expressed frustration with this response, warning that NATO may face a “very bad future” if allies do not support the effort, framing their refusal as a failure to share burden in a crisis rooted in collective energy security.

With allied support lacking, U.S. options to reopen the strait range from continued independent military operations—including expanded attacks on Iran’s navy and missile launchers, mine countermeasure deployments, and targeted strikes on Iranian systems threatening traffic—to multilateral but non-combat measures such as enhanced coordination through the International Maritime Organization (IMO) to establish “safe corridors” or protective frameworks for merchant shipping. Indeed, a proposal supported by the United States and several countries aims to establish such a corridor to assist tens of thousands of seafarers stranded in the Gulf due to the crisis. However, without allied naval contributions, U.S. forces alone risk overstretch, particularly in mine clearance and persistent escort operations.

In the longer run, the war and the challenge of reopening Hormuz are likely to reshape maritime security architectures in the Middle East and beyond. For the United States and its partners, there may be increased emphasis on dedicated multinational maritime security frameworks for strategic chokepoints, potentially separate from NATO’s traditional European focus. The reluctance of NATO members to join a combat mission outside Article 5 collective defense highlights limits in the alliance’s scope and may prompt discussions about new security structures or expanded mandates for naval cooperation in critical global commons. This crisis could accelerate U.S. efforts to strengthen bilateral and regional security agreements with Gulf Cooperation Council (GCC) states, India, and other key maritime powers to ensure freedom of navigation and protect energy supply lines.

The war also underscores the need for a more resilient global energy architecture, pushing consumers and producers alike to diversify supply routes and reduce strategic concentration around chokepoints. This might include expanded investment in pipelines that bypass key straits, enhanced strategic petroleum reserves, and alternative trade corridors such as overland routes through Central Asia and the Caucasus. The scale of allied reluctance to engage militarily also suggests that U.S. leadership in global security may need to balance unilateral action with diplomatic coalition-building to maintain long-term partnership cohesion. Ultimately, the conflict’s pressure on alliances like NATO could catalyze institutional introspection on burden sharing, strategic priorities, and how collective action is marshalled when global economic interests—such as secure energy routes—are at stake.